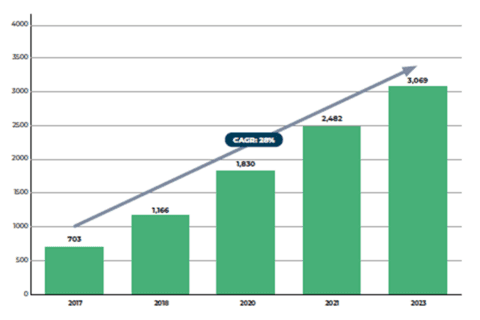

Study: Fintech ecosystem in Latin America and the Caribbean exceeds 3,000 startups

5 mins read

nripn

inEditorial team at FintechBits.

Related Posts

Grove Galaxy Facility: Risks for Crypto Lending

July 21, 2026

Tradable Private Credit: 3 Risks on Stellar

July 21, 2026

DTCC Tokenized Securities: 5 Proven Market Wins

July 21, 2026