We Asked 4 Industry Leaders: How Does Supply Chain Finance Prevent SME Supplier Failures?

Read MoreMarket Insights—Charitarth Sindhu—March 30, 2026

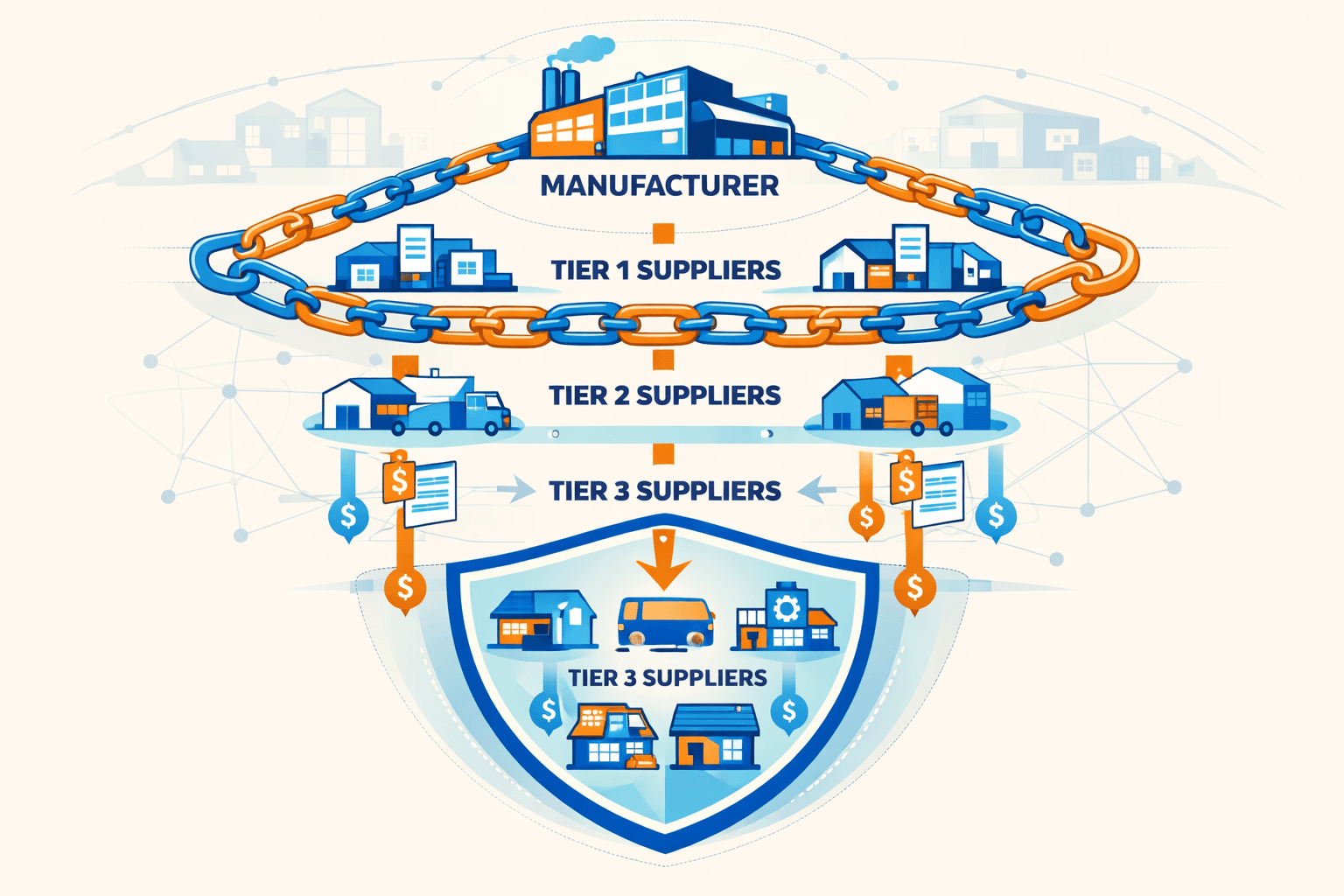

Supply chain finance keeps small suppliers alive by closing the gap between delivering goods and getting paid. Yet most supply chain finance programs only reach tier-1 suppliers, leaving the deeper tiers to fend for themselves. So we asked four industry leaders a straightforward question: what role does deep-tier supply chain finance play in preventing SME