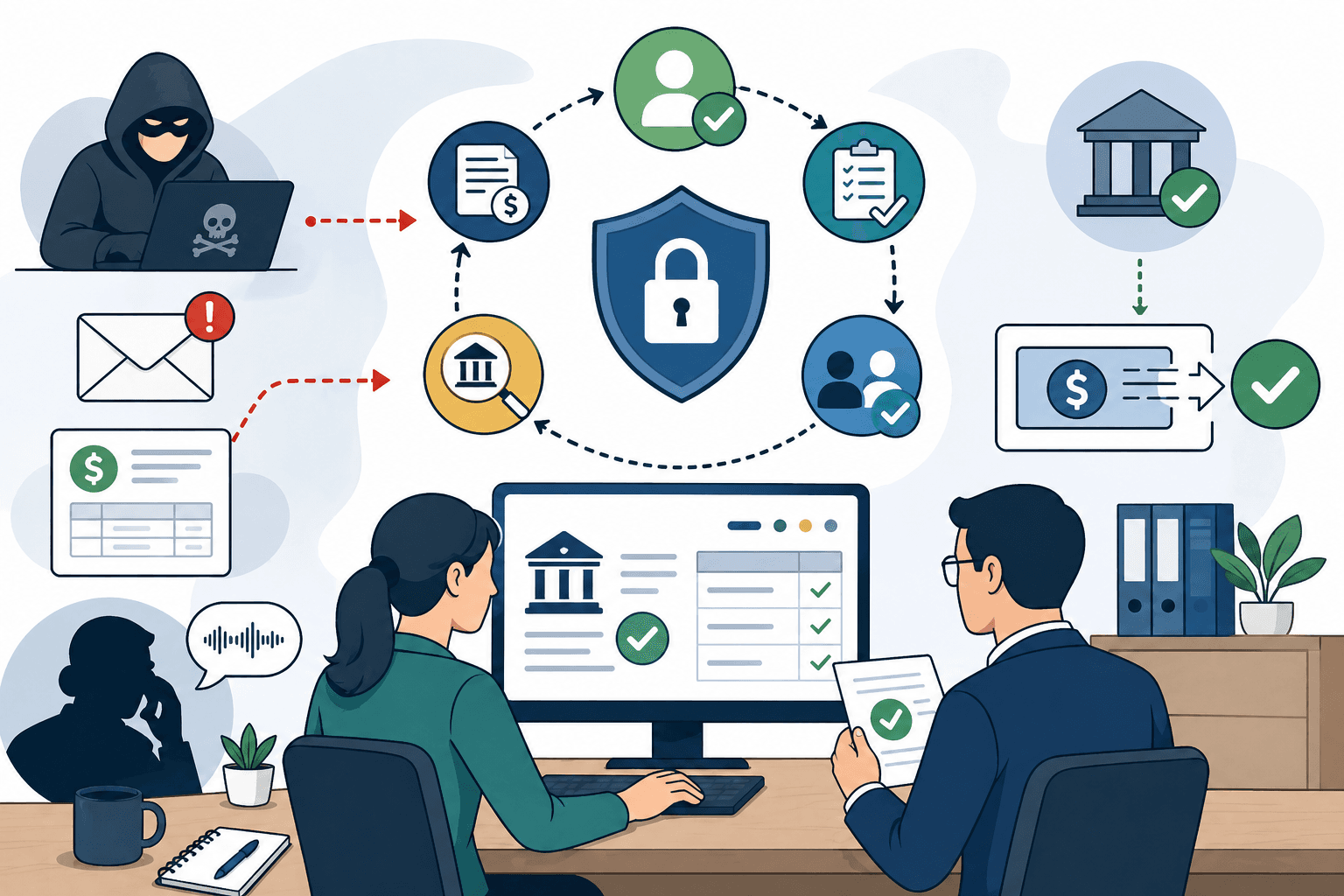

The $55 Billion Blind Spot: Why Your B2B Payment Controls Are Still Built for the Last Decade’s Fraudsters

Read MoreMarket Insights—Charitarth Sindhu—April 28, 2026

Author: Pratik Singh Raguwanshi, Manager, Digital Experience, LiveHelpIndia B2B payment fraud has crossed a structural threshold. The FBI’s 2025 Internet Crime Report recorded $3 billion in business email compromise losses for the year alone, with cumulative BEC damages now exceeding $55 billion since 2013. The 2025 AFP Payments Fraud and Control Report found 79% of organisations