Stay ahead in fintech — Weekly insights, deals, and updatesGet Updates

July 17, 2026

Octus MCP Connector is the company's answer to a question every financial data vendor is now facing. Octus, the credit intelligence platform used by financial, legal, and advisory firms tracking distressed debt and private credit, has launched a connector that lets subscribers query its data directly inside Claude, ChatGPT, or any other large language model

April 2, 2026

Author: Charitarth Sindhu, Fractional Business & AI Workflow Consultant A fractional CFO fintech specialist does something a traditional, full-time CFO structurally cannot. They build compounding insight from navigating financial complexity across multiple regulated companies at the same time. That distinction matters more than most founders realise. Because the fintech landscape moves fast, burns cash faster,

By Jesse Fowler, Founder of J&J Renovations and J&J Plumbing Services Payday Super is about to change every payment cycle for every employer in Australia. If you run a trades business and you have not started preparing for Payday Super, you are already behind. On 1 July 2026, every Australian employer will be required to pay superannuation at the

Fintech jobs 2026 are drawing record interest from professionals across finance, technology, and compliance backgrounds. The global fintech market is projected to reach $334 billion this year, and that expansion is creating demand for highly specialised talent. Recent industry data shows roughly 26,000 fintech job openings worldwide in early 2025, sitting just 18% below the

Fintech internships give student-athletes a direct route from competitive sport into financial technology careers. Three Marquette University Golden Eagles proved this during their summer placements at Fiserv, a global payments leader headquartered in Milwaukee. Sayla Lotysz, Josie Bieda, and Teddy Wong each turned their athletic discipline and academic training into standout contributions. All three have

SME financing remains one of the most pressing economic challenges for developing nations in 2026. Small and medium enterprises account for over 90 percent of businesses worldwide, yet the gap between what these firms need and what they can access keeps widening. According to the International Finance Corporation, the MSME finance gap now stands at

Sign up on Finjobsly.com to get AI-matched to your next Fintech role

Join Finjobsly

Feathery AI decisioning just got funded by the people it automates. Feathery, which builds an AI operating and decisioning system for insurance and wealth management firms, has raised $30 million in total funding including a recently closed Series A led by Portage Ventures. The round drew Index Ventures, Clocktower Ventures, and Bain Capital Ventures, alongside

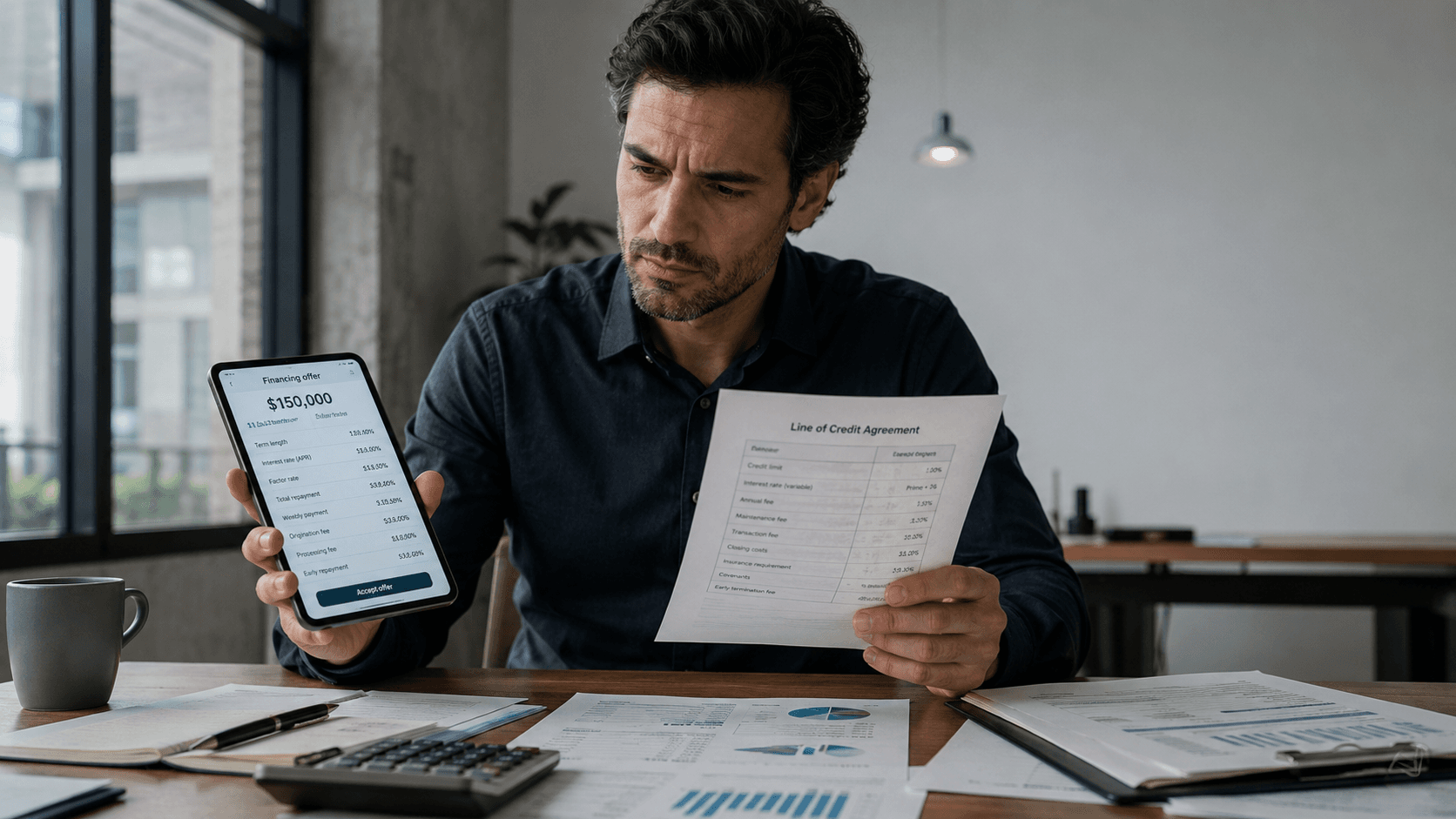

Every business owner has felt the pull of a low headline rate. We asked three industry leaders a blunt question. How can an owner judge whether fintech lending costs genuinely come in below a traditional bank line of credit? Every answer pointed past the advertised APR. Fintech lending costs live in the math behind the

Whoa, speak about a blockbuster transfer within the biotech world! Gilead Sciences simply dropped the information that’s acquired everybody buzzing: they’re shopping for out Arcellx for a whopping $7.8 billion. This isn’t simply any deal—it’s all about dashing up a promising new remedy for a number of myeloma, a tricky type of blood most cancers.

Tilly's Q4 Earnings Beat sent TLYS stock up more than 60% in after-hours trading on March 11, 2026. The youth-focused retailer posted total net sales of $155.1 million for fiscal 2025 Q4. That figure came in comfortably ahead of the $148.7 million Wall Street consensus. Net sales rose 5.3% year-over-year despite the company operating with

Elliott Jana Activist Moves dominated mid-February 2026 headlines as both firms unveiled major positions within days of each other. On February 17, Bloomberg reported that Jana Partners had taken a stake in payments processor Fiserv. Then on February 18, Elliott Investment Management disclosed a position of more than 10% in Norwegian Cruise Line Holdings. Together,

Hank Payments Stock Surge of 639% on February 18, 2026 closed at CAD 0.26 on the TSX Venture Exchange. The microcap fintech now operates as The FUTR Corporation (TSXV: FTRC) after its April 2025 rebrand. The session saw 663,000 shares change hands against a 17,086 daily average. Notably, the relative volume of 38.80 highlighted just

Get the latest news from fintechbits.

Advertisement

◔1 mins read

Modern Treasury Depa Finance is a customer-logo announcement, not a product launch. Modern Treasury said this week that Depa Finance, a stablecoin-native cross-border payments provider, has picked its infrastructure to orchestrate payments across US bank rails and stablecoins. Depa says it processes more than 14,000 payments a day and over $1 billion a year across

◔1 mins read

Axos Arc Technologies is a deal about where digital banks go next. Axos Financial has agreed to buy Arc Technologies, a fintech that gives venture-backed startups a single dashboard for cash management, yield, and debt financing. Terms were not disclosed. The purchase runs through Axos Nevada Holding, a subsidiary of Axos Financial, and the deal

◔1 mins read

Neobank profitability has become the defining test for digital banks. For a decade, these apps chased sign-ups. Now the market wants earnings. Research from Simon-Kucher found that fewer than 5% of the world's roughly 400 neobanks have ever reached breakeven, and most earn under $30 per customer each year. The neobank profitability gap is the